Payday Super in 2026: Why When Your Super Gets Paid Matters

On 1 July 2026, Australia’s superannuation system gets its biggest operational change in decades.

For over 30 years, the Superannuation Guarantee (SG) let employers wait a long time before paying: they only had to put mandatory super into your fund at least once every quarter.

Payday Super ends that delay. Under the new rules, employers must follow the same rhythm as your pay: your super must be paid when you get your salary or wages, and it must reach your fund within 7 business days of payday.

I have been waiting for this change for a long time. With quarterly super, I was always wondering when the next deposit would land — checking my fund balance, doing the mental maths, hoping my employer had actually paid on time. Now that super must move with your salary, that background noise goes away. I can open my account and watch the balance tick up steadily with each pay run. That alone is worth something.

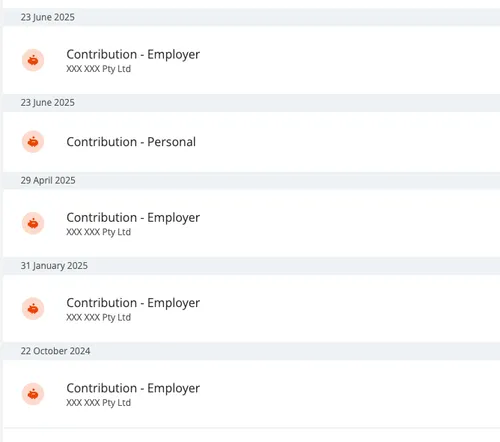

See how random it is for employer contributions landing in my account on FY24/25:

Here’s why that timing change can affect how much you end up with at retirement — and why it also takes a weight off your mind.

🔒 One Less Thing to Worry About

Quarterly super created a gap that was easy to ignore until something went wrong. If you were made redundant, or your company shut down, any super they had not yet paid was at risk. You might spend months chasing unpaid contributions through the ATO while trying to land your next job — on top of everything else going on.

Payday Super does not remove that risk entirely, but it shrinks the window. Your super is paid as you earn it, not batched up in your employer’s account until the end of each quarter. There is less to track, less to chase, and less sitting unpaid if the worst happens. For most people, that is a quiet but meaningful peace of mind.

📉 The Cost of Waiting: Quarterly vs. Monthly

Under the old rules, an employer paying quarterly could legally hold on to your January super until 28 April before sending it to your fund. During that gap, your money sits idle while your employer keeps the cash — and your super fund misses time in the market.

Let’s compare two paths for someone on a $100,000 salary with a 12% SG rate ($12,000 per year), assuming a balanced fund returns 7.5% per year on average:

- Old way (quarterly): $3,000 paid at the end of March, June, September, and December.

- Payday Super (monthly): $1,000 paid at the end of each monthly pay run.

💰 How the Numbers Stack Up

The chart below projects your super balance month by month over 3 years. Both lines use the same 7.5% annual return compounded monthly — only the payment timing differs.

Super balance: monthly vs quarterly payments in 3 years

$100,000 salary · 12% SG · 7.5% p.a. compounded monthly

Both schedules contribute $36,000 over 3 years. With the same monthly compounding rate, monthly payments finish at $40,083 ($4,083 interest) vs $39,841 for quarterly ($3,841 interest) — $242 more from getting super invested sooner.

Even over just a few years, getting super paid monthly instead of quarterly adds extra growth — not from higher contributions, but from your money being invested sooner and you don’t need to do anything to make it happen. The difference is small at first, but it compounds over time. That gap will continue to grow as long as you keep working and contributing.

Of course, the chart assumes a steady 7.5% return. In reality, markets move up and down all year, and none of us control that. A strong year will widen the gap between the two lines; a flat or rough year will shrink it. The exact dollar difference is never fixed.

What you can control is where your money sits while you wait🧘🏻♀️. With this new changes, each pay run shows up in your super account — you can see it, track it, and know it is invested on your behalf. No more guessing whether this quarter’s payment is still sitting with your employer. Under the old quarterly rules, the same money could linger in a company account for weeks or months, earning nothing for you, until someone got around to paying it. That is not a life-changing sum in any single year, but over a working life it adds up — and more importantly, it is your money working for you, not parked on someone else’s balance sheet.